The Noise

The Bank of England raised UK interest rates by 0.5% to 4%, signalling that rates may now be nearing their peak. The US Federal Reserve similarly raised its target for its benchmark rate by 0.25% to a range of 4.5% to 4.75%, with the Fed committee also showing signs that the end of the hiking cycle may be in sight. The European Central Bank lifted interest rates by 0.5%, taking it to 2.5%, as its governing council intends to raise rates by another 50 basis points in March.

According to the Nationwide Building Society, UK housing prices fell for the fifth straight month in January. The average property cost last month was £258,000, down by 0.6% in December and only up 1.1% from January last year. Strong economic headwinds and the unaffordability of mortgages will continue to make it difficult for the housing market to regain any momentum in the near term.

Four hundred and seventy-five thousand union members were on strike in the UK on Wednesday, 1st February, the worst UK strike in a decade. Almost 9% of schools were shut as a result, as several of the major train stations in London were closed entirely. This mass strike also saw civil servants across 124 government departments, London bus drivers, and university lecturers take part in a stand over pay not keeping pace with inflation.

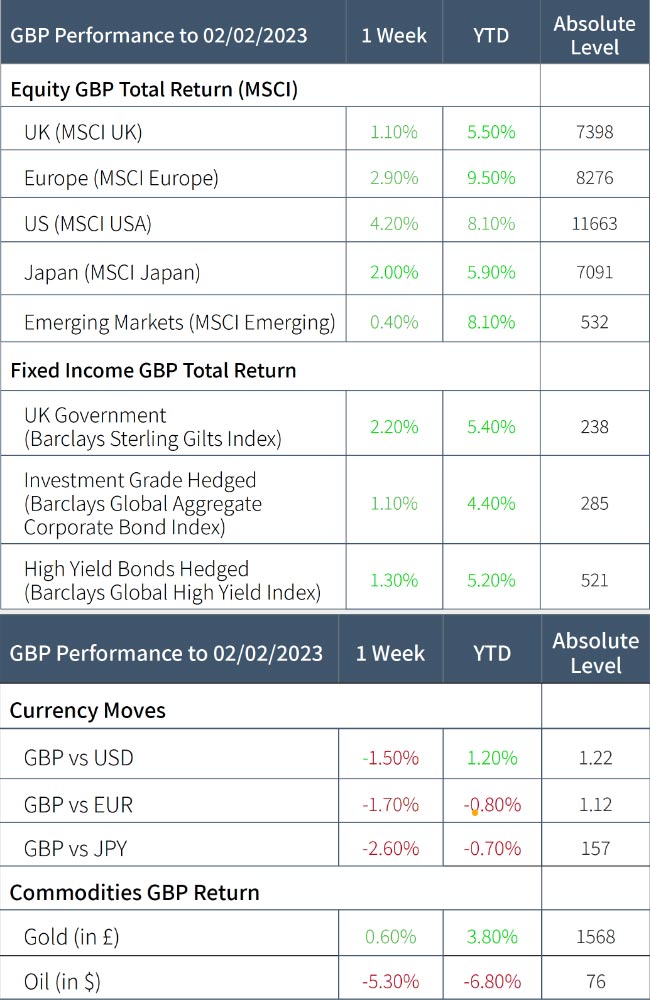

The Numbers

The Nuance

Expectations of a soft landing continue to build as investors extrapolate short-term trends and selectively pick through the data. As corporate earnings reports for last year arrive along with forward guidance for this year, the Manager has seen a continuation of the trend for analysts to downgrade earnings expectations. Very little earnings growth is expected for 2023, and should the trend continue, profits may turn out to be lower than last year. World trade volumes have declined, global manufacturing surveys indicate contraction, US home sales have collapsed, and corporate restructuring announcements are standard.

In contrast, there are many resilient data points. The official unemployment number in the US is still below the historically natural unemployment rate, and consumer credit continues to grow at double digits. US home prices have yet to decline, and the US government continues to engage in deficit spending at record levels. After last June’s explosive CPI increases, the subsequent five months’ official inflation figures have increased at an annualised 1.88%, providing the spark of hope that the fight has been won.

While it is possible that Consumer Price Index growth continues to moderate, this may be a transitory period of lower price rises. The US is on course for a final increase to 5% interest rates in March, likely to be sustained unless the economy deteriorates rapidly. The fixed-income market view of Central Banks pivoting to cut rates this year seems misplaced against the equity market view of a soft landing.

In times of such uncertainty, it is wise to keep an open mind relating to the future and to ensure that your long-term investment plan succeeds under a broad array of possible outcomes.